SCFO #013: Navigating Solopreneur Taxes, Part 1

Read time: 4 minutes

Today’s focus is to help you gain confidence over your taxes.

While I can’t guarantee you’ll love paying taxes any more than you already do 😉, I am sure that if you follow this guide, you’ll be better prepared for taxes in 2023.

Unfortunately, most solopreneurs won’t invest time to understand taxes even though it is their single largest expense.

I get it. Taxes are boring, appear complex, and take time to understand.

But good news!

The aim today is to simplify the complex topic of taxes so you have a better understanding.

Let’s dive in.

Understanding Taxes for Solopreneurs

To understand taxes, you must first understand the different taxes at play as a solopreneur.

The major distinctions are generally based on whether your business is an:

S-Corporation, or

Sole Proprietorship / Single-Member LLC (SMLLC).

To clarify, an SMLLC can elect to be taxed as an S-Corporation.

When I refer to an SMLLC, I’m referring to an SMLLC that has not made an S-Corporation election and is a disregarded entity for tax purposes.

A disregarded entity reports income and expenses on Schedule C of your personal tax return (just like a sole proprietor).

On the other hand, an S-Corp reports income and expenses on a separate tax form (1120-S) and reports that income to the owner on Schedule K-1 to pick up on their personal tax return.

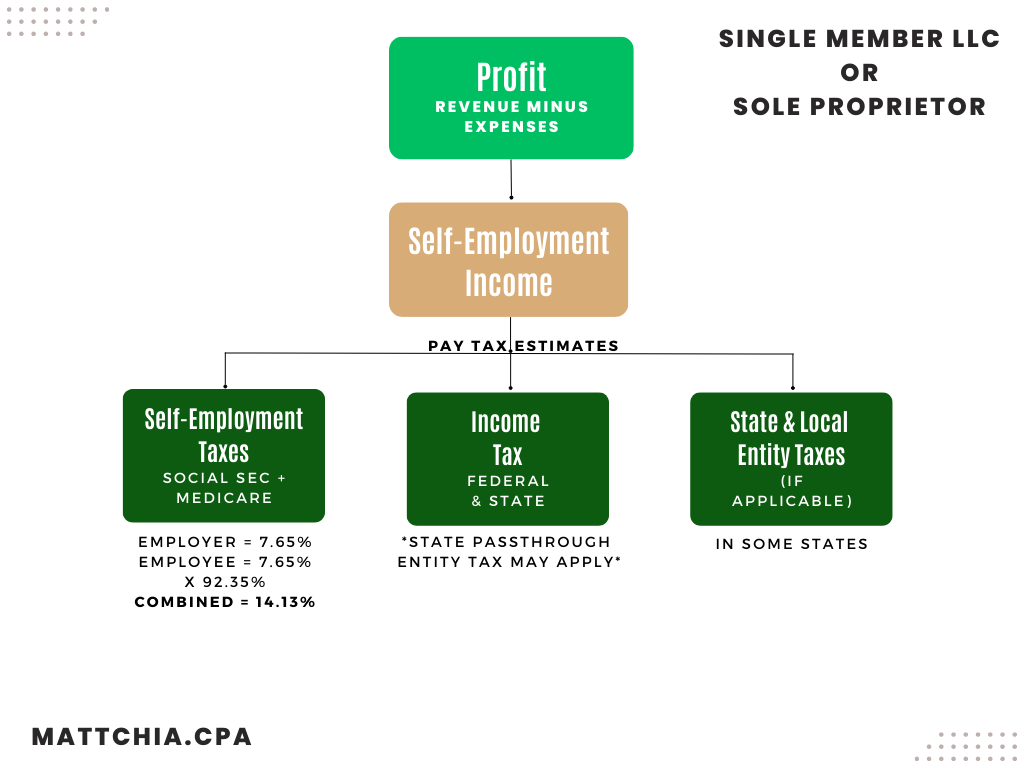

S-Corporation vs. Sole Proprietorship / Single-Member LLC (SMLLC)

Let’s compare a chart of the tax obligations for each structure.

Note: Profit from an S-Corp is broken down between owner W-2 wages and net income because S-Corps must pay a reasonable wage to the owner for work performed.

Now, let’s pivot to owners of an SMLLC or Sole Proprietor.

You’ll notice a few differences between the two charts:

S-Corp owners are subject to unemployment taxes, while self-employed individuals are not.

Self-employment income taxes (14.13%) for SMLLC and Sole Proprietors are slightly lower than S-Corp payroll taxes (15.3%).

Only S-Corp owner wages are subject to FICA taxes, while the remaining business income is not.

Federal and state income tax is withheld on S-Corp owner wages, while self-employed individuals cover these taxes with quarterly estimates.

Some states have an entity-level tax, like Illinois' 1.50% "replacement tax" on net income for S-Corporations and partnerships.

Phew!

That was a lot to digest, but if you've managed to understand these two charts, you'll be better informed than 99% of solopreneurs.

The breakdown should help you understand the various tax categories at play that are often mixed up by solopreneurs, and understandably so.

What Causes Surprise Tax Bills?

Tax surprises typically occur because federal and state income taxes are underpaid.

Throughout the year, you make estimated taxes for federal and state income taxes, and if you’re an S-Corp owner, you also withhold federal and state taxes on your paycheck.

The combination of tax withholding and tax estimates represents how much you paid for federal and state taxes, but not necessarily how much you owe.

How much you owe is dependent on your net business income (PLUS owner’s wages for S-Corp owners and any other income outside of your business).

To provide an example, let’s say you owe $20,000 in federal and state taxes based on the income you earned.

If you paid estimated taxes of $5,000 and withheld $10,000 from your paycheck, you’d owe $5,000 when you file your tax return.

Not a fun result for anyone involved.

But this can be avoided, and we’ll cover that next week in part 2.

When to Pay Estimated Taxes

You may not know this, but CPAs generally use a safe harbor when they provide you with estimated taxes.

A safe harbor is the government’s way of saying that if you pay close to what you owed last year OR your expected liability for the current year, you won’t be on the hook for underpayment penalties or interest.

99% of the time, CPAs use last year’s taxes to figure out the safe harbor estimates you pay during the current year.

For example, if your total tax obligation was $20,000 last year, your CPA might have you pay $5,000 each quarter.

Note: you’d pay 110% of last year’s tax bill if you filed jointly with your spouse and had adjusted gross income > $150,000 or > $75,000 if you’re single or file separately. You can also meet the safe harbor by paying estimates on 90% of the current year's tax liability.

If your income increases and you use last year’s safe harbor for your current year's taxes, you could be in for a surprise when you file your taxes.

Federal taxes are due under the following schedule:

This means you’ll want to review your income earned during each of these “quarters” to determine how much you owe.

Not all states follow this same schedule, but most do.

Now that you have a better understanding of how and when to pay estimated taxes let's quickly summarize the key takeaways from this article.

TL;DR

As a solopreneur, it's crucial to understand the differences in tax obligations based on your business structure (S-Corp, SMLLC, or Sole Proprietor).

Surprise tax bills often result from underpayment of federal and state income taxes throughout the year.

To avoid unpleasant surprises, be aware of the safe harbor rules when paying estimated taxes and monitor your income during each quarter.

Familiarize yourself with the due dates for federal taxes and state taxes (if applicable) to ensure timely payments.

By following these guidelines and staying informed, you'll be better prepared for taxes in 2023 and less likely to face any unexpected tax bills.

In part 2, we’ll discuss how to make tax surprises a thing of the past.

P.P.S. if you’re a solopreneur and want to minimize taxes while maximizing financial clarity, book a free 15-minute call today.

Let me help you get unstuck in your personal and business finances, so you can focus on doing what you love.

Disclosure: please consult with your CPA, Attorney, or Advisor to execute this strategy. I am a CPA, but I’m not your CPA.